🔮 Why I changed my mind on self-driving cars

The exponential tipping point is here

This essay was last edited on 30/08/2024 to account for the latest news (Wayve's collaboration with Uber) and JPM research report on Waymo's unit economics in San Francisco

When people ask me to describe my work, I say I take a critical look at exponential technologies. This also includes critically reviewing my own analysis.

So here’s a reflection: I have long argued that self-driving cars were metaphorically miles away from being a reality, a tonic to the rah-rah hype that its makers were foisting upon us through marketing.

KITT, the car from Knight Rider, will remain the gold standard for autonomous vehicles.

Autonomous vehicle pilots will become increasingly ambitious, but the real-world hurdles will still take time to navigate, even with friendly city regulators. None will ship to the public in 2018.

Four years later, I was equally pessimistic about the potential of self-driving vehicles. In 2022 I wrote in Exponential View:

Max Chalkin analyses the disappointing trajectory of full self-driving efforts: $100bn invested and little to show. Self-driving pioneer, Anthony Levandowski who cofounded Waymo, has retreated to building autonomous trucks constrained to industrial sites. He reckons that is the most complex use-case the technology can deliver in the near future. (Amazon has also abandoned its autonomous delivery robot programme.)

Why it matters: Self-driving could be a pointless distraction for improving the environmental and human impact of transport. It takes attention away from micromobility, better urban infrastructure and other strategies to improve the safety, pollution, climate, equity and economic returns of this sector.

That was then and this is now. KITT remains awesome and I’m changing my mind about self-driving cars. Far from being a “pointless distraction”, they’re nearly ready for prime time.

That’s not just based on a hunch. It’s based on an increasing mountain of evidence pointing to their adoption and evolution – and the evidence that overlapping S-curves are beginning to form around the industry. My experience being driven around by a Wayve self-driving car in chaotic London streets helped a great deal too. In this essay, I’ll explain how I’m thinking about the development of self-driving based on evidence I have access to and the frameworks of the Exponential Age.

Wheely big growth

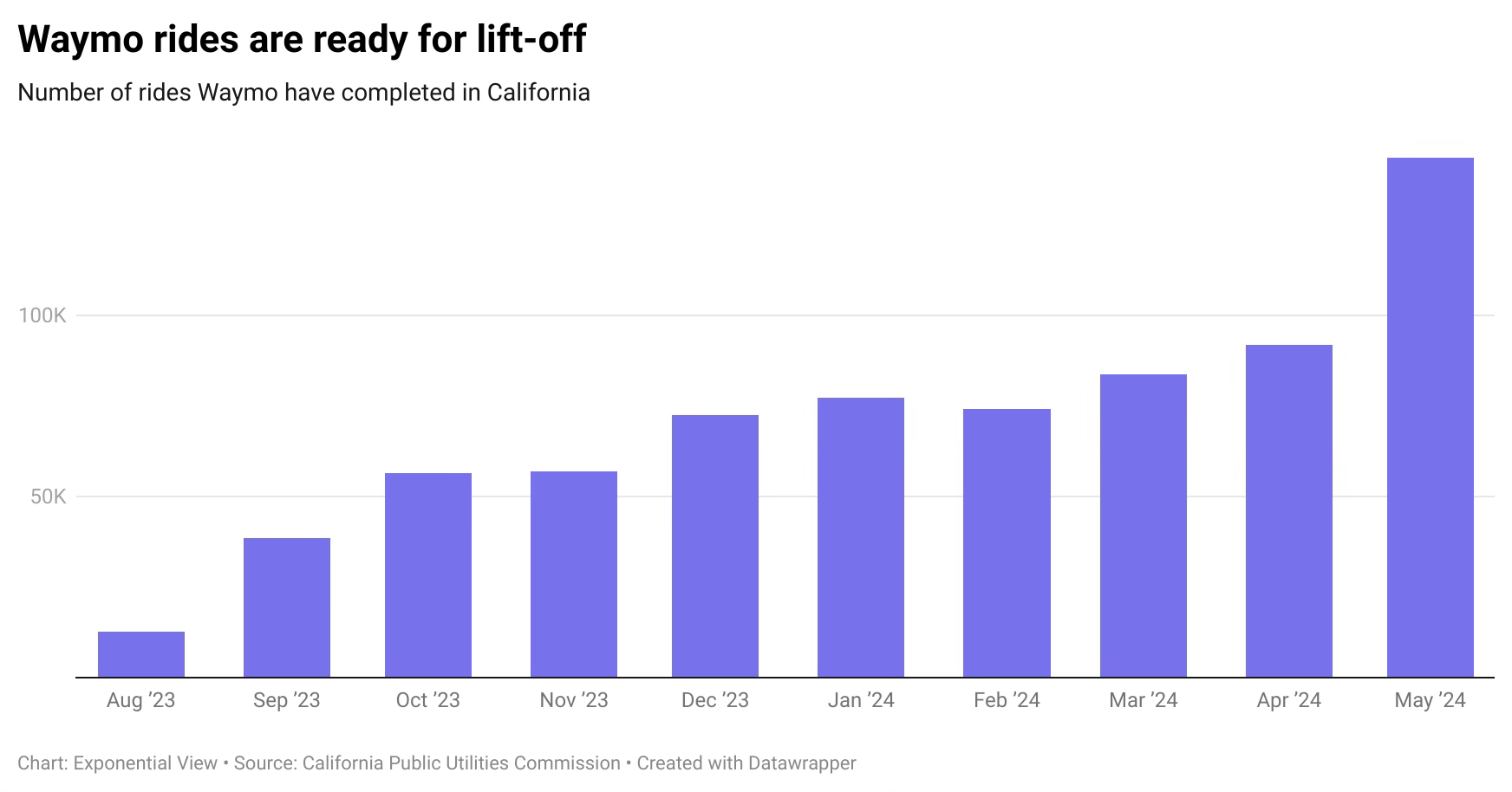

In bellwether cities, which have historically been ahead of the curve on tech adoption, we’re seeing more self-driving vehicles on the roads, behaving normally (for the most part, but more on that later). Robotaxis, in particular, are spearheading this revolution. San Francisco has seen a tenfold increase in Waymo rides taken in the past ten months. In Wuhan, a city desiring to become “the world’s first driverless city”, around three in every 100 taxis are robotaxis, developed by Baidu Apollo.

As Waymo expands beyond San Francisco, so do its numbers: earlier this month, it said it provided 100,000 paid rides a week across San Francisco, Los Angeles and Phoenix. The company doubled its ride volume in just two months.

These numbers highlight how quickly robotaxis can grab market share. While it’s not clear what proportion of Waymo’s 100,000 weekly rides happens in San Francisco alone, the city is their most mature market, so it is likely the bulk of rides.

That gives us a direct comparison with Uber’s staffed rideshare service, which runs approximately 200,000 rides a day in San Francisco. Given Waymo’s 100,000-a-week figure, the company likely offers 10,000 or more rides a day in the city, a 5%-ish or more market share. This is close to the tipping point of an S-curve of adoption of 6%.1

Waymo’s ride numbers would also give San Francisco a justifiable claim to be the world’s first “driverless city”. Waymo has a larger number of rides per day in San Francisco than Baidu does in Wuhan – despite the Chinese city having a population ten times larger. Wuhan, however, leads by driving the cost of robotaxi journeys down. A 10-kilometre ride in a robotaxi in Wuhan is between a fifth and half the price of a ridesharing equivalent. Anecdotally, a ride in Waymo in San Francisco costs around 20% more than an Uber.

Without driver fatigue, the number of rides a robotaxi can run a day can be greater than that of its non-automated predecessor. In Wuhan, robotaxis complete up to 20 rides a day, which matches or even exceeds the average of 13.2 for human taxi drivers in the city.

What about the economics? Baidu operated around 336,000 Apollo Go rides in July. This means that Baidu Apollo could be netting $200,000 to $800,000 a month or $2.5-10 million a year. The Apollo, costing only $28,000 to build, is much cheaper than Waymo’s cars, which are estimated to cost $150,000.

Baidu Apollo looks likely to reach profitability before its American peer. The firm expects unit economics to breakeven this year and profits by 2025. Researcher Amber Zhang points out that some analysts are suggesting breakeven within Wuhan this year. But Waymo still has a path to profitability. If Waymo can improve its current utilisation rate of 35% to match Uber’s (55% in New York), it could see a 58% revenue increase at high margins, boosting investment returns from ~0% to over 30%.

However, they will face an incoming challenge from the incumbents. Wayve has recently announced a partnership with Uber. There may be a few bumps in the road for Waymo.

Selling self-driving to suburbia

Of course, history is littered with tomorrow’s technologies that saw adoption and excitement among early adopters but didn’t cut through to the masses. Yet here too we see evidence that self-driving vehicles – in their initial form of robotaxis – are starting to burst out of the tech bubble.

Waymo is expanding its self-driving taxi service as regulators become more accepting of autonomous vehicles. Already established in Phoenix and San Francisco, Waymo has recently launched in Los Angeles and Austin. The company is also testing operations in 25 major metro areas, including Atlanta, Houston, Dallas and Miami. Of course, Waymo is cherry-picking cities with favourable conditions for autonomous vehicles. Regardless, all of this is signalling the increasing acceptance of self-driving technology in urban transportation.

Beyond robotaxis, the public is becoming more comfortable with the tech, too. My hypothesis remains that Tesla is far behind the likes of Waymo when it comes to self-driving, but its ubiquity is helping normalise acceptance of the tech. Full self-driving is available to drivers all over the US and Canada and is expected to roll out in China by the end of this year. The more people get hands-on – or hands-off, as the case may be – with the tech, the more willing they are to overcome worries and prejudices about it.

But to accept this, tech first needs to address major concerns. In October last year, a pedestrian was first hit by a human-driven Nissan, then struck and dragged 20 feet by a Cruise self-driving car on a San Francisco street. This event led to Cruise losing its operating permit in California and ceasing operations in Arizona and Texas. It was an awful accident and a moment of reflection for the self-driving car sector.

Exceptions can often make rules. The Cruise accident was an exception. It caused reflection. But the fact is that cars are getting safer. For some road users, self-driving vehicles are preferable to those piloted by humans because their actions are more predictable. Some cyclists already say they feel safer biking next to a Waymo car than human-driven vehicles.

For good reason: Waymo’s performance, as measured by miles per disengagement (when a human has to take control) has been improving in the long run:

My experience in a Wayve car in London may be instructive here: the car managed to smoothly traverse a tricky situation with loads of police cars, as well as a wobbling Deliveroo driver veering from lane to lane.

Changes in perception

We have two overlapping S-curves here, which add up to true technological innovation and exponential growth. First, we have the S-curve of technology improvement.