💭 The real reason tech companies want regulation

Clarence isn’t from the 313.

You couldn’t have missed it. The world’s largest tech companies have started to clamour for regulation in this hugely under-regulated sector. So I’ve taken a moment to pen some thoughts. I’d love your comments. And feel free to forward this to a friend.

On Monday, Sundar Pichai of Alphabet wrote in The FT:

there is no question in my mind that artificial intelligence needs to be regulated. It is too important not to. The only question is how to approach it.

He followed up on this in a trade event in Brussels where he called for a moratorium on facial recognition:

Facial recognition is fraught with risks. I think it is important that dominant regulation tackles it sooner rather than late. It is important that governments are involved. It can be immediate but maybe there’s a waiting period before we really think about how it’s being used.

I was in Brussels at the time with Microsoft’s President, Brad Smith, chatting about a similar topic. Brad has written a book, Tools and Weapons, on the dual-sided nature of our current crop of technologies and why they need certain controls.

Brad calls for greater regulatory oversight of these key technologies and complementary characteristics, such as AI, content moderation and privacy. (Brad and I had a conversation which we’ll feature in the EV podcast in a week or two.)

Why are these companies calling for regulation of technologies now?

The tech industry got a speed-up with the Intel 4004 processor, launched in 1972. This was contemporaneous with American right-leaning economists launching a sustained attack on the regulatory state. The growth of the early PC industry in the late seventies and early eighties coincided with the supply-side thinking of Reagan and Thatcher. As an industry, it has enjoyed the fruits of limited government oversight. But tech was a nuclear reactor running hot because we had not only taken the control rods out, we had pooh-poohed them as antithetical to the purpose of the reactor. That reactor now seems to be doing a full-blown Chernobyl on us.

So, of course, now it makes sense to investigate the nature of these digital innovations, how they form part of the architecture of our daily lives, how they come to market, who controls them and their heteroskedastic affects on different groups. We need to ask whether the interplay of these technologies with society and market forces has led to organisations having new classes of power, or simply too much power, and whether there are appropriate safeguards and processes, including judicial ones, in place.

Brad brings much of this to life in his book, from his recounting of dealing with the Snowden revelations and the aftermath of the Christchurch massacre, amongst others. It was clear that this book is a well-intentioned, robust and honest effort to get democratic governments involved in governing these technologies, rather than leaving it exclusively to the management of these firms.

But…

Of course, there is a but. There are three buts, actually.

If you know you are going to be pwned, you may as well do it to yourself. B-Rabbit showed us how it is done in 8 Mile.

Regulation is coming to the tech industry. I’ve written about that extensively over the past four years. (See, this interview in The Times for example.) A smart strategy would be to help facilitate the debate, which is what Microsoft and, to a lesser extent, Google is doing. An aggressive one, which may yet prove to be smart, is to foment hostilities—an us vs. them attitude. This seems to be Facebook’s unrepentant approach.

The second but is that regulation favours large companies. Regulation is complicated. Dealing with it means dealing with lawyers, hiring compliance people, changing your product roadmap, building new code. Regulation raises barriers to entry. The most regulated industries, finance and health, have seen the deep consolidation and weak flow of new entrants for decades. Regulation favours the large. (Just look at how publishers struggled to get to grips with GDPR across their websites. I ran a product group in a large European publisher. We had dozens of people, product managers, researchers, engineers and others, involved in building our privacy layer. Our company was tiny compared to Google.)

Tech stalwarts are upended or rendered irrelevant by competitors. Not by regulation and rarely by horizontal entry into the market. Microsoft and the PC era did for Sperry, Burroughs, Wang and the mainframers. Salesforce knocked Siebel on the head. Netscape threatened Microsoft’s dominant position. Facebook thrashed Google+ and So.Cl, the social network efforts of Google and Microsoft.

Regulation could advantage the strong at the expense of the new entrants being able to regulate the incumbents in the market via competition. Regulation is an irritant to a trillion-dollar firm, it’s a pre-existential issue for a founder thinking about her new startup.

The real question of regulation

We clearly need to have new rules of engagement around our technosphere. There are emergent properties that we have to tackle because we do have to deal with deep fakes, viral hate content, cyber vulnerabilities, authoritarian AI, and more. These threaten our individual liberties and the functioning of our societies. Moderating them through some form of regulation, perhaps of the agile, experimental type Brad Smith proposes doesn’t seem wholly unreasonable.

Now to the third of the three buts I promised you. The technology companies are not talking about the other thing that needs to be regulated: large, AI-driven, platform-network companies. This is a simple point of power and scale. Microsoft reaches 1.5bn consumers, which makes it small compared to Google, Apple or Facebook, all of whom reach larger bundles of humans.

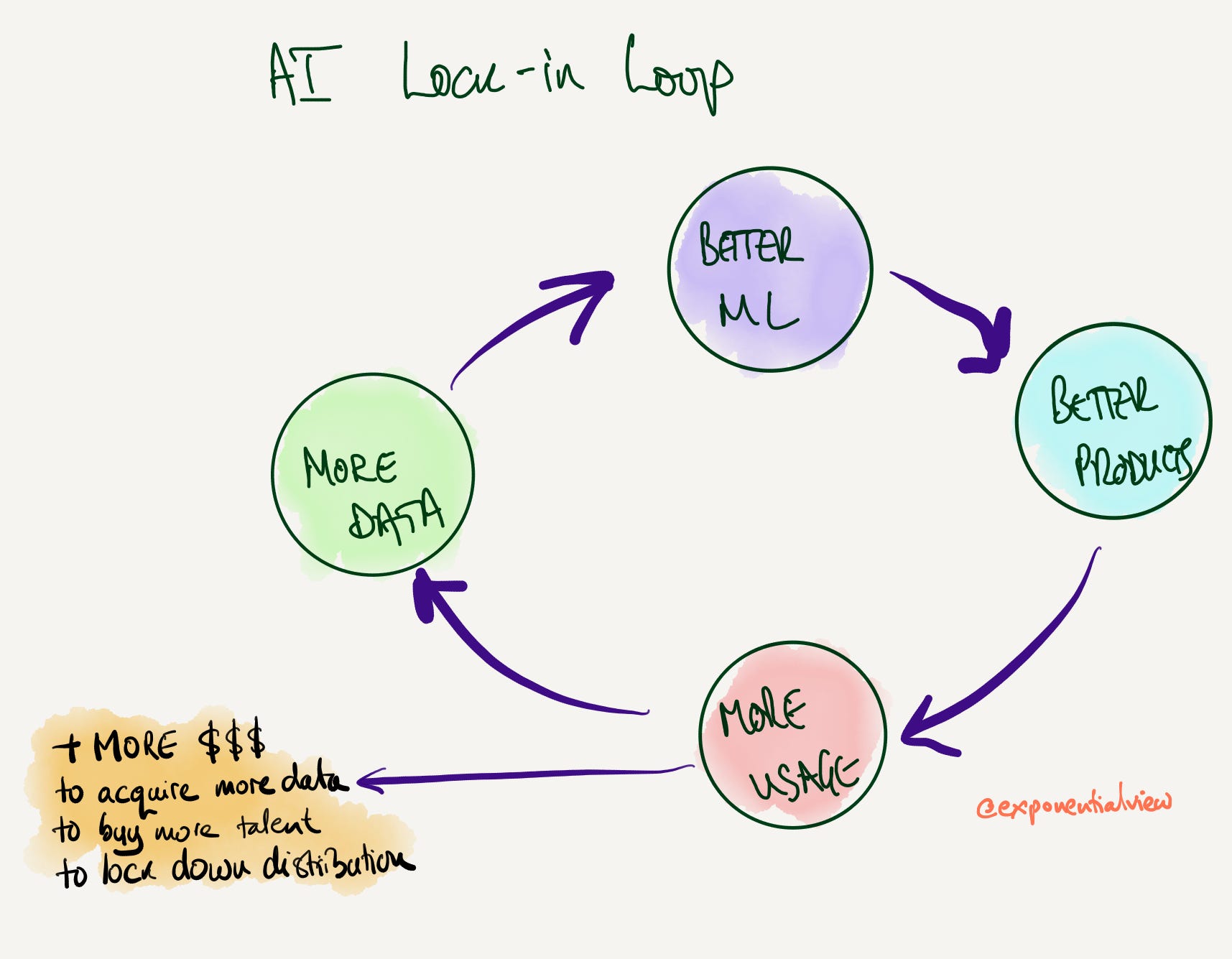

In the exponential age, the engine at the heart of our leading companies, is the perpetual motion machine, the self-blowing windmill, of artificial intelligence. What I have for years called the AI lock-in loop: data begets AI, begets better products, begets more data, begets better AI, begets better products.

In the industrial age, companies faced, at some point, diminishing marginal returns. They didn’t really get much bigger because distribution became expensive, markets became saturated, competitors could compete. Expanding horizontally was also hard. Analog assets and skills were not as fungible and interoperable as digital ones.

Not so in today’s digital hubs, with their ability to aggregate data into a single platform. Google has been hoovering up data to feed its engine for a decade. Microsoft did the same with its acquisitions of LinkedIn and Github (less than $35bn the pair.) They can step into ancillary businesses because software has eaten the world, and data feeds it.

It isn’t simply data network effects, which most manifestly power dominance in the search-ad-surveillance business of Facebook and Google. It is the traditional network effect of platforms, the strength of the partner ecosystem they can build, which strengthens their platforms too.

The bigger these platforms get, the bigger they can get. Like some fearsome creature at the boss level of a coin-op arcade game. Or, more soberly, like the chart below from Iansiti and Lakhani, two Harvard profs.

In the decade leading up to 2019, the largest 100 firms in the world increased their total market cap by $12.7trn, according to PwC. Of this, $4.2trn, a quarter, was accounted for by just seven: Amazon, Apple, Alphabet, Microsoft, Facebook, Tencent and Alibaba.

Market cap is only one metric. But, size means power. Power of our politics, power to rewrite norms, power over our lives. And power that comes without democratic accountability.

It isn’t clear there is any proximate limit to how big these companies can grow. Imagine a Google or Apple or Microsoft twice the size it is today, exceeding a quarter of a billion dollars of revenue a year. Microsoft grew at an annual rate of 7 per cent or so in the decade to 2019. But since 2017, it has grown at 15 per cent per annum—and its profit margins have widened. That level of growth extended over five years would double Microsoft’s size. If Facebook’s growth rate slows to 25% per annum for the next five years, it will treble in size—to $200bn in revenue. It’s plausible that Amazon could puncture $500bn in revenues by 2024. So how big could these MAFAAs (Microsoft, Apple, Facebook, Amazon and Alphabet) ultimately become? What are the implications if they become that big?

The concentration of big tech goes hand in hand with their financialisation. And the complex choreography of ownership that shuffles around IP rights, licensing obligations, the domicile of their revenue and ultimately the tax they pay. (See this article that documents Netflix’s intricacies.)

The playbook of the digital firm, riding high on these network effects, is to create a monopoly. As Peter Thiel says in Zero to One, tech pioneers should set out to create a

“monopoly” […] the kind of company that’s so good at what it does that no other firm can offer a close substitute. Google is a good example of a company that went from 0 to 1.

These monopolies have been good for the consumer, driving down prices and driving up product quality. Google is a great search engine, better than its rivals (Quaero, Exalead, Webcrawler, AltaVista.) Facebook was a better social network than MySpace, Plurk, Orkut, Friendster or Ryze. And because network effects are often pretty good for consumers, courtesy of Metcalfe’s Law, these tech giants confuse regulators which look for consumer harm to justify taking action against monopolists. The behemoths repeatedly lie to themselves by denying their monopoly status.

But Thiel’s notion of monopoly also has a specific requirement about the creative dynamic that brilliant tech firms should live in.

In a static world, a monopolist is just a rent collector [...] But the world we live in is dynamic: it’s possible to invent new and better things. Creative monopolists give customers more choices by adding entirely new categories of abundance to the world.

The question is what steps will these large firms take to ensure the world isn’t dynamic? And to what extent will the AI perpetual motion machine keep them ahead? Raising regulatory costs deters competitors. AI’s lock-in loop advantages incumbents.

Do these particular characteristics allow for the creation of the fecund environment for the dynamic competition to keep a Thielian monopolist in check?

If they aren’t kept in check by competition, then what will? What will the limits to the big tech firms’ power be?

And the only answer then might be government, the state, the regulator, unfashionable though it may be to say. And knowing that, a decent strategy for any large tech firm is the ‘woke’ one, focus on emotive and important issues early, such as facial recognition. So that we don’t ask the really hard questions.

Love your thoughts,

Azeem

P.S. EV reader, Mark Bunting, who read a draft of this made the point that I sound like I’m arguing for the break up the big tech companies. I’m not really going that far. I am suggesting that they need to start talking about the issues their scale raises and whether they see limits to how large they ought to get. And that we need to have a clearer discussion about the very different roles they play as utility entities, pseudo-security players, owners of the public space, providers of consumer and business services and R&D vehicles.

Dig deeper

My conversation with Brad Smith is available from Feb 5th on our podcast channel.

David Runciman, Professor of Politics at Cambridge University, and I talk about the superhuman capacities of large companies, how that may clash with the state and democratic politics.

Binyamin Applebaum and I discuss some of the historical aspects of the rollback of the US regulatory state.

“And the only answer then might be government, the state, the regulator, unfashionable though it may be to say. And knowing that, a decent strategy for any large tech firm is the ‘woke’ one, focus on emotive and important issues early, such as facial recognition. So that we don’t ask the really hard questions.” I believe *we* do need to ask the really hard questions, Azeem, which takes courage because governments are seen as unfashionable. Otherwise, the critical spirit is blunted and weakened much the same way as the ‘woke’ strategy you outline is weak.

The postscript is interesting. I don’t think it’s sufficient for the tech companies and their satellites/dependents alone to have the conversation about scale. I’d like us to take very seriously the threat implied in Thiel’s depiction of monopoly, because I’m not convinced that all dynamic states will engender competition.

The key question is, “what regulation?” One pernicious impact of the libertarian reshaping of the regulatory debate that you describe is that we talk about companies being “regulated” or “regulated.” All the digital platforms are subject to a host of regulation. It’s obviously ineffectual to address important problems, as implemented today. The real problem, though, isn’t the lack of rules; it’s the intellectual poverty of regulatory visions. Even GDPR is a refinement of the basic approach staked out in the 1995 Data Protection Directive. In the US, we’re grasping back to Progressive-era antitrust, which is well and good. It’s just not going to be sufficient. We’ll need new conceptual approaches to regulation for the novelty of this environment, just as we did in earlier periods.

Also, you’re obviously right that the embrace of regulation by big tech CEOs is strategic. However, something has changed quite substantially in the zeitgeist over the past five years. The rhetoric that regulation and innovation are inherently incompatible (and innovation is obviously superior) is no longer viable in polite society. You may still hear it from Peter Thiel, but even Zuckerberg makes concessions to reality. So there is reason for hope.